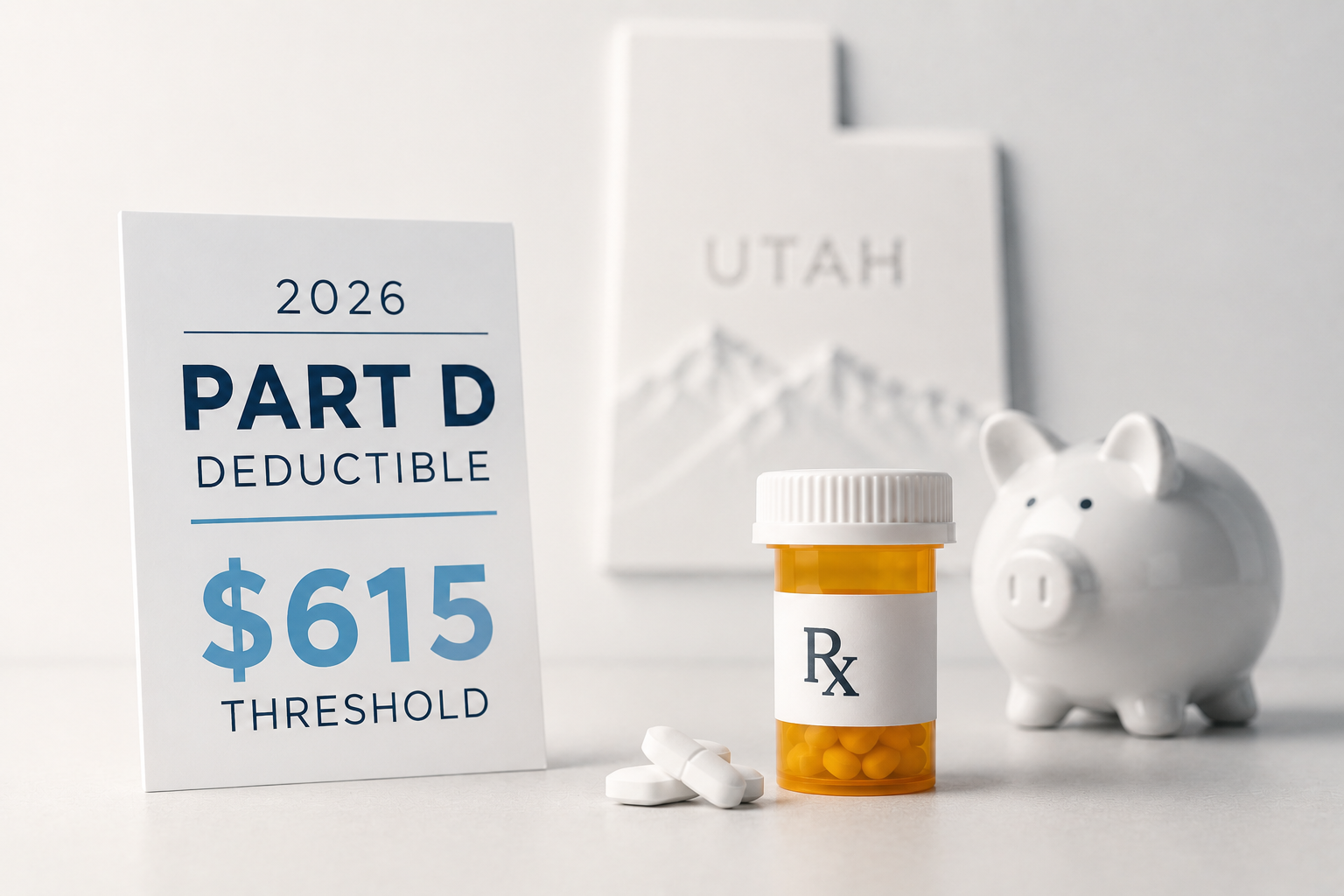

Heading the 2026 Medicare plan year, Utah’s 395,242 Medicare beneficiaries are facing a restructured landscape of prescription drug costs. While the new $2,100 out-of-pocket cap has garnered significant attention, it is equally important to understand the "front end" of your coverage: the annual deductible. For 2026, the Centers for Medicare & Medicaid Services (CMS) has set the maximum standard Part D deductible at $615.

Understanding how this $615 threshold operates within the 55+ Medicare Advantage and standalone drug plans available in Utah is critical for your financial planning. Whether you're living in the high-growth retirement communities of Washington County or the urban center of Salt Lake County, the deductible is the first hurdle in your journey toward the pharmacy counter.

What is the $615 Part D Deductible?

In simple terms, a deductible is the amount you must pay out-of-pocket for your prescription drugs before your Medicare plan begins to pay its share. In 2026, the maximum allowed deductible has increased to $615.

remember, not every plan in Utah uses the full $615 amount. Our analysis of the Utah Market Logic 2026 data reveals that carriers compete aggressively by offering "enhanced" plans that may feature a $0 deductible or a reduced deductible for specific drug tiers. But for many standalone Prescription Drug Plans (PDPs) and lower-premium Medicare Advantage plans, the $615 threshold is the standard starting point.

The Impact on Utah’s Urban and Rural Enrollees

The way a deductible affects your wallet often depends on where you live and which carrier you choose. In Utah, we see a distinct divide in how these plans are utilized:

1. The Wasatch Front (Salt Lake, Utah, Davis, and Weber Counties)

In high-density areas like Salt Lake County, which holds 137,549 enrollees, competition among carriers like UnitedHealthcare (H4604) and SelectHealth (H5216) is fierce. Many of these carriers offer Medicare Advantage plans with a $0 deductible on Tier 1 and Tier 2 drugs. This means that if you only take common generics for blood pressure or cholesterol, you may never actually have to pay the $615 deductible. Your coverage begins on day one.

2. Rural Utah (Sevier, Duchesne, Uintah, and beyond)

For the 28,372 enrollees living in Utah’s rural counties, standalone Prescription Drug Plans (PDPs) are often a primary choice. These plans, such as those offered by Wellcare (S4802) or SilverScript (S5884), almost universally apply the full $615 deductible to all brand-name medications. For a senior in Richfield or Vernal taking a brand-name medication, the first $615 of their drug costs in January will likely be their full responsibility.

How the Deductible Interacts with the $2,100 Cap

One of the most common questions we receive is: "Does my $615 deductible count toward my $2,100 out-of-pocket limit?"

The answer is Yes. Every dollar you pay toward your $615 deductible is credited toward your $2,100 annual out-of-pocket cap.

The Math: If you pay your full $615 deductible in January, you only have $1,485 remaining in out-of-pocket spending before you hit the "Catastrophic Phase" and pay $0 for the rest of the year.

For high-utilizers of specialty medications, such as those treated at the Huntsman Cancer Institute or Intermountain Medical Center, this means they will move through the deductible phase very quickly, hitting the $2,100 cap often by the end of the first quarter.

Strategic Selection: $0 Deductible vs. Lower Premiums

During the 2026 enrollment season, Utahns will have a choice. Do you choose a plan with a monthly premium but a $0 deductible, or a plan with no premium but a $615 deductible?

Case A (The Maintenance User): If you only take generic drugs, a plan with a $0 deductible on Tiers 1 and 2 is important. This ensures you never have to "buy-in" to your coverage.

Case B (The Specialty User): If you take a drug like Eliquis or Jardiance, you will pay the $615 deductible regardless. In this case, it might be more beneficial to choose a plan with a $0 monthly premium, even if it has the full deductible, because you are guaranteed to reach the cap anyway.

Carrier Spotlight: How the "Big Three" Handle Deductibles in Utah

UnitedHealthcare (H4604): With the largest enrollment in Utah, United often features a "Tiered Deductible." In many of their 2026 Salt Lake plans, the deductible only applies to Tiers 3, 4, and 5. Tier 1 and 2 generics are typically exempt.

SelectHealth (H5216): As a local Utah carrier, SelectHealth frequently matches its deductible structure to the needs of the Intermountain Health patient base. We often see $0 deductibles on common maintenance medications to encourage medication adherence.

Humana (H1994): Humana’s 2026 strategy in Utah continues to focus on value. Their standalone PDPs often utilize the full $615 deductible but offset this with lower co-pays once the deductible is met at their "Preferred Pharmacy" networks.

Conclusion

The $615 deductible is not a hidden fee; it is a structured part of the Medicare Part D benefit. By understanding how this threshold applies to your specific medications, you can avoid surprises at the pharmacy in January. Whether you're in the heart of the Wasatch Front or the quiet of rural Utah, a careful audit of your plan's deductible structure is the first step in a successful 2026 enrollment.

2026 Medicare Key Numbers At A Glance

Sources: CMS 2026 Parts A & B Fact Sheet (Nov 14, 2025); SSA 2026 COLA Fact Sheet; CMS 2026 Part D Redesign Program Instructions.

Social Security COLA, 2020 to 2026

Source: SSA COLA history; 2026 COLA Fact Sheet.

Sources

- CMS, 2026 Medicare Parts A & B Premiums and Deductibles Fact Sheet (Nov 14, 2025): Part B standard premium $202.90; Part B deductible $283; Part A inpatient hospital deductible $1,736.

- SSA, Social Security Announces 2.8 Percent Benefit Increase for 2026 (Oct 24, 2025) and 2026 COLA Fact Sheet: 2.8% COLA; average retired worker benefit rises from $2,015 to $2,071.

- CMS, Final CY 2026 Part D Redesign Program Instructions: $2,100 annual Part D out-of-pocket cap.

- 2026 IRMAA brackets (single $109,000 / joint $218,000 starting thresholds); Part B IRMAA total ranges $284.10 to $689.90/month; Part D IRMAA surcharges $14.50 to $91.00/month. See CMS 2026 Fact Sheet (linked above) and the Kiplinger 2026 IRMAA brackets summary.

- CMS, Medicare Part D Prescribers by Geography and Drug: state and local prescription totals and costs (2023 release).

- CMS, Medicare Care Compare: nursing home, hospital, dialysis, and home health quality ratings.

- Utah Department of Health and Human Services, dhhs.utah.gov: Utah-specific provider and health workforce data.

A note on sources: This article references publicly available data from CMS (Centers for Medicare & Medicaid Services), the Utah Department of Health and Human Services, and the Kaiser Family Foundation. Specific carrier filings reference the 2026 plan year CMS landscape data.

This article is for educational purposes only. Nothing here is medical advice or specific financial advice. Talk to your doctor and a licensed Medicare advisor before making decisions about your coverage. This content is not connected with or endorsed by the U.S. Government or the federal Medicare program.

CMS 2026 TPMO Disclosure: "We do not offer every plan available in your area. Currently we represent 15 organizations which offer 55 products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program (SHIP) to get information on all of your options."